As investors look to diversify their fixed income strategies, an integrated and holistic approach can make a big difference.

Traditional investment grade public fixed income investments are a mainstay of institutional portfolios, and the same can be said of investment grade private credit to some degree, depending on the investor’s goals. In an ideal scenario, an investor might see a benefit to these two elements of their fixed income strategy being integrated in both spirit and execution – the left hand knowing what the right hand is doing, you might say. At SLC Management, the public and private fixed income teams work together to deliver investment grade long-duration strategies to a range of client types. To understand the upside potential of this for investors, II spoke with SLC Management’s Rich Familetti, Chief Investment Officer, U.S. Total Return Fixed Income, and Sam Tillinghast, President, U.S. Private Fixed Income.

You both run long-duration portfolios. Where are you seeing interest in your strategies from investors at the moment?

Rich Familetti: On the public fixed income side, we are seeing a strong demand for designing and managing liability-driven investment (LDI) strategies. We have a long history of delivering both traditional and customized solutions for clients, and it continues to be a growth area for us across the board, particularly among corporate defined benefit (DB) plans. We manage portfolios across the duration spectrum and have seen strong excess returns across almost all of our strategies. In the long duration space, we’ve had good performance while consistently providing the proper risk profile required to hedge long duration liabilities. In public fixed income markets, we’ve been able to consistently find mispriced or undervalued securities, and that’s a result of a team-oriented and hands-on approach between our portfolio managers and credit analysts.

Sam Tillinghast: On the private fixed income side, we focus on opportunities in investment grade private credit, which is a newer asset class to many investors. This segment of fixed income has higher yields than comparable public bonds, and financial covenants and collateral securing the loan. These are issuer and transaction types that you don’t normally see in the public markets, so they provide additional diversification. Traditionally, the asset class has been dominated by insurance investors to back their long-term liabilities. At the moment, we are seeing a lot of interest from smaller insurance companies looking to outsource part of their balance sheet and to pick up additional yield for comparable credit quality. And we’re seeing corporate pension plan sponsors who are looking for additional yield and diversification versus their traditional public credit allocations. Overall, on the investment-grade private side, we’re more of a spread shop than a volume shop. That leads us to move into more niche areas than other insurers, and away from more of the traditional types of privates.

You both mentioned DB plans. What roles to you see DB plan sponsors expecting of traditional public fixed income and private credit?

Familetti: Corporate defined benefit pension liabilities are typically discounted using high-quality corporate bond yield curves. So, investment-grade corporate bonds, and treasuries to a certain extent, have been the natural home for most liability hedging assets. That has been a source of demand as more plan sponsors have looked to de-risk their plans. Sponsors certainly need to be active in managing those assets, in part because the discount rate is drawn from such a narrow universe. Liabilities aren’t subject to downgrades or defaults, so it’s important to diversify and have an active strategy around long-duration assets to keep pace with the liabilities.

Tillinghast: We think that high-grade public bonds will continue to form the majority of most DB plans’ portfolios. Investment-grade private credit should be thought of as a high-quality complement to provide diversification in sources of alpha. We’re focused on more complex and often structured transactions within investment grade private credit. We’re typically getting 50 to 100 basis points over equivalent public bonds, with historically lower losses than the publics. That’s due to the covenants and collateral that I mentioned previously. That additional spread reflects the complexity of the deals and the lower liquidity of private markets. While it is true there’s not as much liquidity as there is in publics, we think investors are typically over compensated as the lower liquidity really reflects a lack of sellers, not a lack of buyers. I’ll add that DB plans are long term in nature and generally have the capacity to give up some liquidity on a portion of their portfolio.

It sounds as if there’s a role for both public and private credit in liability-hedging portfolios?

Familetti: Absolutely, and as a good example, we manage the Sun Life U.S. corporate DB plan using a combination of public and private credit in a customized LDI framework. Our allocation to private fixed income is currently in the 15-20% range, and that goes back to what Sam mentioned about private fixed income being a good diversifier with the right sort of duration characteristics to seamlessly integrate into that LDI framework. Private credit also has a volatility profile very similar to A and AA corporate bonds that make up the methodology for determining discount rates. So, it’s a good asset class that adds some extra income without going down in quality and works well in a liability-hedging strategy.

Since you mentioned insurers: risk transfer is a hot topic of the moment. How do insurers view private credit in a pension buyout?

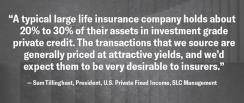

Tillinghast: Insurers tend to be very comfortable with private credit – in fact, you could say they are the most comfortable with it of all investors. A typical large life insurance company holds about 20% to 30% of their assets in investment grade private credit. The transactions that we source are generally priced at attractive yields, and we’d expect them to be very desirable to insurers.

Can you describe some of the similarities and differences in how you approach the public and private spaces?

Familetti: I think both teams look to source good relative value through really digging into the securities we purchase and through looking for areas that are undervalued. We also both utilize some of the broader SLC Management resources, such as the Global Research Team. The biggest difference is that public fixed income markets require a significantly more active strategy when you consider the technicals of the market. The public markets are generally more volatile than the private side, given the number of participants that can push bonds around and have an impact on value over a comparably shorter horizon. We’re really looking to exploit relative value across individual securities or across sectors of the market. The breadth of the public markets means that we’re able to find undervalued – and avoid overvalued – issues that can provide good risk adjusted returns for our clients.

Tillinghast: In the private markets, we’re always comparing the transactions that we do to equivalent public bonds in the context of relative value – the additional spread that we pick up at issuance when we initially buy the transaction. We look for niches where we have deep expertise. For example, areas such as aviation or financials are often avoided by other investors. One of the most important parts of private credit, however, is the origination or sourcing of transactions. A small amount of privates trade in the secondary market, so you must identify the opportunities when they first come to market. To do that requires a wide range of strong sourcing relationships that allow you to see a good variety of transactions. If you’re not called by that placement agent or intermediary when that deal first comes to market, you’re unlikely to have the opportunity to invest. In other words, relationships are extremely important for private markets.

It’s often thought that information and data are harder to come by in the private credit space. Is that the case?

Tillinghast: Certainly, there’s less publicly available information on transactions in privates. That said, in terms of underwriting transactions, we’re often able to obtain more information on our issuers than is typically available in the public markets. As these transactions are confidential, the issuers will provide any credit or financial information that we request. There’s also a much longer timeline for private transactions and we’re able to spend weeks, sometimes even months on due diligence. You could make the argument that private lenders actually have more information when it comes to underwriting the transaction.

In terms of valuation, you’re comparing the private transactions to other private transactions that have recently come to market – but also to what’s happening in the public markets, and you’re adding a premium for the private transactions depending on the type. A typical corporate transaction in the private market would be valued at 20 to 25 basis points more than a comparable corporate in the public bond market. And if the deal is structurally complex, you might add over 100 basis points, this is the end of the market we’re generally looking at.